Powering the Future: The Role of Automotive Battery Wholesale Distributors in the EV Revolution

Introduction The electric vehicle (EV) revolution is underway, transforming the automotive industry and reshaping how we think about transportation. Central to this shift is the advancement of battery technology, which powers these innovative vehicles. As the demand for EVs accelerates, automotive battery wholesale distributors play a vital role in this evolving landscape. Understanding the EV Market Landscape The global push for sustainable transportation options has led to a surge in EV adoption. Factors such as governmental regulations, increasing fuel prices, and consumer awareness of environmental issues are driving this trend. By 2030, millions of EVs are projected to be on the road, creating an immense demand for high-quality automotive batteries. The Importance of Wholesale Distributors Wholesale distributors are crucial in the automotive supply chain, bridging manufacturers and retailers. They ensure that the battery supply matches the growing demands of the EV market. Here are some key roles they play: 1. Ensuring Product Availability With the rapid increase in EV production, distributors must maintain adequate stock levels of batteries from various manufacturers. This ensures that automotive retailers and service stations can readily access the necessary components to meet consumer demand. 2. Facilitating Partnerships Wholesale distributors foster partnerships between battery manufacturers and automotive companies. By connecting these entities, they help to streamline the supply chain, improve product quality, and facilitate innovation. 3. Providing Technical Support Battery technology can be complex, and wholesale distributors often provide technical assistance and training for retailers and service technicians. This support is essential for the effective installation, maintenance, and troubleshooting of EV batteries. Challenges Facing Battery Distributors While the role of wholesale distributors is vital, they face several challenges in the transitioning automotive landscape: 1. Supply Chain Disruptions The COVID-19 pandemic highlighted vulnerabilities in global supply chains, affecting battery production and distribution. Distributors must navigate these challenges to ensure steady supply. 2. Evolving Technology Batteries are at the forefront of technological innovation, with continual advancements in energy density, charging speed, and sustainability. Distributors need to stay updated with these trends to remain competitive. Future Opportunities for Wholesale Distributors As the EV market continues to expand, wholesale distributors have greater opportunities to innovate and expand their services: 1. Embracing Sustainability Distributors can play a key role in promoting sustainable practices by sourcing eco-friendly batteries and adopting greener logistics methods. 2. Expanding Product Lines With the emergence of new battery technologies, distributors can diversify their product offerings to include cutting-edge options such as solid-state and lithium-sulfur batteries. 3. Leveraging Technology Utilizing technology such as data analytics and inventory management systems can help distributors optimize stock levels, predict trends, and enhance operational efficiency. Conclusion As we move towards a more sustainable future, automotive battery wholesale distributors will be crucial enablers of the EV revolution. Their role in ensuring product availability, fostering partnerships, and providing technical support cannot be overstated. By adapting to challenges and seizing new opportunities, these distributors can power the future of transportation in an era defined by electrification.

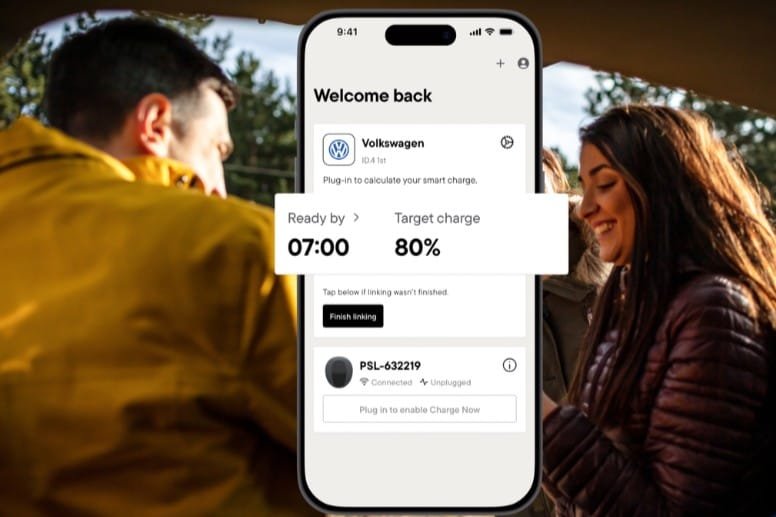

Pod Point rebrands to Pod; launches charging subscription

For an upfront cost of £99 and a monthly subscription fee of £40, subscribers will receive a Solo 3S charger, installation to their home, and a 48-hour Service Level Agreement. No additional tariff will be charged beyond the customer’s home energy bills and the subscription fee. Pod states that all customers will have to do is plug their vehicle in at home, and it will be smart charged to a target level by a specified time such as 100% by 7AM. Pod will then also provide cashback to customers covering ‘smart-charged’ miles at a rate of 2.3p per mile up to either 5000 or 7500 miles per year, which the company states could result in an annual payout of more than £170. One of Pod’s main claims is that signing up to Pod Drive will cut up-front installation costs for a charger “from £1,249 to £99”. Examining Pod’s existing website, it shows that the company offers a tethered 7kW Solo 3S charger for £1,149 including installation. Adding surge protection costs an additional £100, so that’s £1249 – although Pod has not confirmed whether Pod Drive includes this additional extra. Then, there’s the monthly charging cost of £14.37, which paid over three years costs around ~£517. The Pod website states that brings up the total cost of buying upfront to £1766.50. Looking at the webpage for Pod Drive, it shows that the subscription entails a three year agreement (36 months). If you pay £40 per month for three years and pay the £99 feasibility fee, then the total cost of the charger over the lifetime of the agreement hits £1540 in total. So, it’s still cheaper than buying a charger up front. Pod states that buying one of its chargers nets you a 5-year limited warranty and a 10 day average response for service, whereas Pod Drive provides a lifetime warranty and a 48hr guarantee. But, the critical element here is that Pod Drive is essentially a lease agreement, and if you cancel your subscription, you won’t get to keep the charger. Pod CEO Melanie Lane said: “Pod Drive takes the hassle and complexity out of going electric and removes significant barriers in the form of upfront costs. As the original innovator in electric charging, we are constantly working hard to make life with an EV easy for drivers. Our EV charging heritage means we are well placed to help households shift to clean energy in a way that also helps the UK’s electricity grid.” Laine added: “Pod Drive is only the first of a number of everyday electrification propositions we are developing as we expand from providing chargers to helping busy households with all their charging needs. With over 250,000 customers already trusting us to be at the heart of their EV life, we see Pod playing a leading role in the UK’s increasingly electrified future.” In a press release, Pod outlined some of these propositions, including a plan to develop its partnership with Tesco to sync drivers’ charging data across home and public charging points, as well as offering Pod Drive to OEMs such as Mazda for their customers. pod-point.com, podenergy.com

Is there a role for second-life batteries before recycling? – pv magazine International

Lithium-ion batteries are everywhere, powering everything from consumer electronics to electric vehicles, residential PV storage systems, and, more recently, mitigating curtailment in large-scale wind and solar power plants. EVs are driving large-scale demand for Li-ion batteries which will result in substantial volumes of spent batteries in the near future. This scenario highlights the potential for repurposing EV batteries for second-life stationary applications, which could maximise their value before recycling. However, to fully realise this opportunity, several economic, technical, and regulatory challenges must be addressed and resolved. May 22, 2025 International Solar Energy Society (ISES) The large majority of lithium-ion (Li-ion) battery production is dedicated to powering electric vehicles, and these batteries will become available for stationary applications typically 5-8 years later. In 2023, electric vehicles accounted for 80% of Li-ion battery demand. Lithium-ion battery costs and prices have been declining rapidly, mirroring the price reductions seen in solar photovoltaics. Li-ion batteries have become dominant in both electric vehicle and energy storage applications, and the significant cost decreases they have experienced recently are due to advancements in technology, economies of scale in manufacturing, and shifts in battery chemistries. As the fast uptake of rooftop PV continues, solar has already overtaken nuclear, large-hydro, coal and natural gas, and will become the largest contributor to the world’s energy mix by the turn of the decade. Increased penetration of PV systems in both transmission and distribution networks can greatly benefit from the balancing capabilities that batteries can provide. Due to the intermittent nature of the solar resource, short-term electricity storage using Li-ion batteries will become essential. As the figure below shows, the cost-reduction curves of both silicon PV modules and Li-ion batteries are similar. In large-scale PV and wind generation, curtailment has become common, and together with overbuilding PV and pumped hydro energy storage, large-scale Battery Energy Storage Systems (BESS) is being widely deployed everywhere. Evolution of the PV module global annual production (in GW, blue bars and left-hand axis), and of the annual average price of PV modules and Li-ion batteries in relation to the average price in 2010 (in %, green and orange points respectively, right axis) (Data from RenewEconomy, BloombergNEF, Fraunhofer ISE, IRENA). Evolution of the PV module global annual production (in GW, blue bars and left-hand axis), and of the annual average price of PV modules and Li-ion batteries in relation to the average price in 2010 (in %, green and orange points respectively, right axis) (Data from RenewEconomy, BloombergNEF, Fraunhofer ISE, IRENA) Image: ISES Second-life Li-ion batteries and the EU Battery Passport A battery that has been retired from its original application, such as in EVs, but still retains enough capacity and functionality, can be repurposed for stationary energy storage applications. Key drivers of second-life battery markets include policies promoting sustainable energy storage and circular economies; collaboration between automakers, battery manufacturers and energy companies; and advancements in battery diagnostics and refurbishing technologies. Advanced battery grading technologies are being developed by several start-ups. These technologies could be in-vehicle end-of-life battery testing to determine battery State-of-Health (SOH) in the order of minutes rather than hours as per typical cycling techniques, reducing testing time and therefore cost. The EU Battery Passport is a digital record that tracks the entire lifecycle of a battery, from raw materials to disposal and recycling. It is a key component of the EU's Battery Regulation, aiming to increase transparency and sustainability in the battery value chain. This digital passport will be accessible and mandatory for specific battery types starting 2027. Industrial batteries (over 2 kWh), electric vehicle batteries, and light means of transport (LMT) batteries (like e-bikes) will require a Battery Passport starting February 2027. Consumers and other stakeholders will be able to access the Battery Passport information through a QR code printed on the battery or its packaging. The EU hopes that the Battery Passport will help to promote the use of sustainable materials in battery production, encourage responsible recycling and end-of-life management, increase consumer awareness and trust in battery products, and facilitate the development of a circular economy for batteries. The EU Battery Regulation entered into force on August 8, 2023. To facilitate the dismantling of batteries and to support repairers, remanufacturers, second-life operators and recyclers in their operations, the battery passports will also contain more detailed data on battery composition, dismantling (such as the tools required for disassembly) and safety measures. This includes values for performance and durability parameters, SOH, battery status (e.g. ‘original’, ‘reused’, ‘waste’), and information related to the battery use (e.g. number of charging and discharging cycles, accidents that the battery may have been subject to). Many players in the battery industry see benefits in focusing on repurposing battery packs, rather than performing disassembly and repurposing battery modules, because labor and cost for disassembly are substantial. A California startup has announced the commissioning of the world’s largest second-life, grid-connected battery energy storage installation. The 53 MWh storage project, made up of retooled EV batteries, has been operating commercially, storing and dispatching power to the grid, since May 2024. The project enabled the reuse of 900 EV batteries to make up the BESS. Asian and European companies have developed the infrastructure, financing, and expertise to handle large volumes of retired batteries across various chemistries and form factors. Despite the example above, the US market remains fragmented and immature. A significant challenge is the disconnect between first-life battery owners and second-life buyers. First-life owners often expect to recoup 50% or more of the original value of their batteries. However, second-life companies typically aim to pay only 10 to 20% of the original price to remain viable. This disparity, coupled with the rapid obsolescence of older battery technologies, creates a mismatch of expectations. Many surplus and lightly used EV batteries are sent straight to recycling — despite being viable for second-life use. This is due to warranty gaps, testing costs, and the falling price of new batteries. Second-life batteries provide a bridge between recycling and disposal, enabling a circular economy in energy storage, but they might only be viable

What Are The Implications Of $66/kWh Battery Packs In China?

The Implications of $66/kWh Battery Packs in China The advent of $66 per kilowatt-hour (kWh) battery packs in China signals a transformative moment for several sectors, significantly impacting the electric vehicle (EV) market, renewable energy adoption, and the broader economy. As one of the largest producers and markets for batteries globally, China's cost reduction in battery technology will have far-reaching implications. 1. Electric Vehicle Revolution Affordability and Accessibility The $66/kWh price point makes electric vehicles more affordable for consumers, effectively narrowing the price gap with traditional internal combustion engine vehicles. With lower battery costs, automakers can either reduce the overall price of electric vehicles (EVs) or enhance vehicle range and performance. This democratization of EVs is pivotal in accelerating their adoption. Competition Among Manufacturers As battery costs plummet, competition among domestic and international manufacturers intensifies. Chinese companies such as CATL and BYD, leading the global battery market, will likely face pressure from global automakers and newcomers. This environment fosters innovation, potentially leading to improved battery technologies. 2. Renewable Energy Synergy Energy Storage Solutions The declining costs of battery packs facilitate broader adoption of energy storage systems, essential for managing renewable energy sources like solar and wind. With cheaper storage, homeowners and businesses can invest in renewable energy solutions, storing excess power generated during peak production times for later use, ultimately promoting energy independence. Grid Stability Utility companies in China can leverage affordable battery storage to stabilize the grid. As renewable energy sources fluctuate, batteries can provide reliable energy during downtimes, optimizing energy distribution and reducing reliance on fossil fuels. 3. Environmental Impact Carbon Emission Reduction Lower battery costs align with global carbon reduction goals. The transition to cheaper EVs can expedite the phase-out of fossil fuel vehicles, considerably decreasing greenhouse gas emissions. Additionally, enhanced storage capabilities support the incorporation of renewables, further diminishing carbon footprints. Recycling and Sustainability Challenges While the initial impact of cheaper batteries is positive, the long-term implications may include increased e-waste. As EV adoption rises, so does the need for efficient recycling systems for spent batteries, necessitating investments in sustainable practices. 4. Economic Growth and Job Creation Industrial Expansion China's battery sector is poised for growth as a result of lower costs. This could stimulate the establishment of new manufacturing plants, leading to job creation in regions focused on battery production and assembly. Global Trade Dynamics Affordable batteries put China in a strong position in international markets, possibly reshaping global trade relationships. As countries strive for energy solutions, China’s dominance in battery technology might grant it greater economic influence. 5. Challenges Ahead Supply Chain Vulnerabilities While lower battery costs present opportunities, they also expose vulnerabilities in the supply chain. Global demand for materials required in battery production, such as lithium, cobalt, and nickel, may lead to resource competition and geopolitical tensions. Quality and Safety Concerns As manufacturing ramps up, ensuring quality control becomes paramount. With pressures to produce affordable batteries swiftly, there’s a risk of subpar products entering the market, potentially affecting safety and performance. Conclusion The introduction of $66/kWh battery packs in China marks a pivotal moment in the evolution of energy and transportation sectors. While it presents tremendous opportunities for advancing electric mobility, promoting renewable energy, and fostering economic growth, it is essential for stakeholders to navigate the associated challenges to ensure a sustainable future. As China continues to lead in battery technology, the world watches closely, anticipating the ripple effects of this transformative development.

China Electricity Expert Talks Wind, Solar, & Storage In The Country

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and/or follow us on Google News! Last Updated on: 20th February 2025, 12:56 pm Recently I had the opportunity to sit down with one of the leading experts on electrical generation in China to discuss the absurd scales of all forms of electrical generation and storage. In the first half of our conversation, we talked coal, gas, and nuclear. In the second half — lightly edited transcript below — we talked wind, solar, and storage. Michael Barnard [MB]: Hi, welcome back to Redefining Energy Tech. I’m your host, Michael Barnard. As always, we’re sponsored by TFIE Strategy, a firm which assists investment funds and firms to pick the winners and avoid the losers in climate solutions. My guest today is David Fishman, senior manager at the Lantau Group and one of the world’s leading experts on what’s happening in China with electrical generation. Join us for the second half of our fascinating conversation. Okay, so that’s the bad stuff. We’ve talked about coal, we’ve talked about natural gas, the fossil fuels. But now let’s pivot to the holy moly stuff that China has been doing with the other stuff. I have a soft spot for wind energy.I’ve gone through most domains of major climate problems and when I started electrical generation was one of the ones I started with. I started by looking at wind and understanding everything about wind energy. I’ve got a real soft spot for the space. It’s going to be not eclipsed, but in the end it’s going to be more solar than wind in the global grid. I had to give up on that idea. But tell us about wind energy in China. It’s just such a fascinating story of extraordinary growth and over the past two. David Fishman [DF]: There’s three kinds of wind that I’ll talk about. One that is pretty mature, one that is maturing and one that is recently emergent that I think is very interesting. So first onshore wind, the mature one. Tons and tons of onshore wind up in the northeast, the north and the northwest. They’ve been building it well since about 2014, 2015, even going before that. But the real big spike came around 2015, 2016. They got into trouble with curtailment at that time. Kind of overbuilt at the moment. The grid wasn’t able to receive that much wind power. They couldn’t operate flexibly. Coal was getting priority in the dispatch queue and kicking wind out, stuff like that. A lot of investors got burnt. 2015, 2016, a lot of foreign investors who had rushed in to build wind in western China and then weren’t getting their subsidies and they sold off all their assets and left swearing to never do China renewable investments ever again. To my understanding, there is at least one investment bank based in Hong Kong which I’ve talked to people at. They say every time I input a new project initiation code in our system and I say that I want to do a renewable project in China, an automated flag pops up that says, have you reviewed the file on 2015, how much money we lost on that wind project in China? Make sure you review that before we continue with this new project. So, you know, they’re aware of it. And then things actually stabilized and tapered off in the last few years. So the onshore wind in what we call the three norths in China, the Northeast and the Northwest, has really not been as aggressive as I hoped, maybe in the last three years or so. Wind capacity growth has still been healthy, of course, and, but for China, it’s been underperforming, in my opinion, versus what could have been. And that’s because I think they’re looking at some really rough interconnection issues that the capacity build out for has exceeded the infrastructure build out. And that still you’re seeing issues with dispatch not being intelligent or flexible enough to accommodate all of these wind resources coming online in what are essentially barren deserts, right. Places with no load. You have to be able to get them into a line, ideally a UHV line, and send them somewhere else where they’re. So that’s been the story of onshore wind doing well. MB: But, but let’s just test this because I hear conflicting stuff. Every year since 2014 I’ve been doing a comparison of nuclear versus wind and solar because it’s just a fascinating variance thing. But what is the actual experience? So what is the degree of curtailment in China these days on the ground as opposed to Western headlines or other stuff? DF: That’s specifically, at this moment, a very pertinent question. In the last few months especially, everybody I know in the industry here is complaining about curtailment. Everybody says curtailment is high out west, and yet the figures on curtailment coming out at the provincial level do not support that. MB: What are the figures? I mean, I was on stage in Brussels and I was hearing horror stories about European curtailment. I’m just trying to get actual capacity factor numbers, you know, that are believable and if anybody has them, it’s you. DF: Officially every province has its own KPIs for curtailment, but they’re supposed to be under 5%. In the last year, several provinces relaxed their requirement and allowed it to go as 10%. Officially no province has higher than 10% curtailment and most of them have no higher than 5% curtailment. Now I believe 100% that is true for the eastern provinces and down south and anywhere that has a large power demand. I have no doubt that they’re wasting very little of their wind power. However yesterday Lauri Myllyvirta at CREA published on what happened in November in China. Why did thermal generation grow in November

Largest BESS in Denmark complete, interconnector backup option

Alongside smaller operational BESS in Kolding, Munkebo and Korsør and a soon-to-be-commissioned project in Svenstrup, North Jutland, EWII will soon have a total BESS fleet of 49MW/82MWh. Claus Møller, commercial director for EWII, said that the company was focusing on BESS as ‘it works’ while other clean energy technologies are facing technological and commercial hurdles. “While large energy projects such as energy islands, wind supply and hydrogen plants are stranded on the drawing board, we are focusing on battery technology because we know it works. With our digital platform, both we and our customers can trade with flexibility, which is why we will invest further in BESS plants and energy storage in the coming years,” said Møller. The Bornholm project could in the future power the island for 1-2 hours if problems arise with a subsea interconnector cable to Sweden, Møller added: “If the submarine cable fails, the battery at Hasle could quickly connect and supply the island while boilers at the local power plant heat up. This is not a current option today, but we hope it will be a solution in the long term.” Other companies deploying grid-scale BESS in Denmark include (primarily) solar developers Better Energy, Eurowind Energy and Nordic Solar as well as BESS developer-operator Dais Energy, with CEO Daniel Connor discussing the market with Energy-Storage.news late last year. Denmark has strongly underlying merchant revenues and there is also talk of bringing in a capacity market (CM), but for now the merchant stack makes financing relatively challenging, Connor said.

BYD signs 3.5GWh BESS supply deal for Grenergy’s Oasis de Atacama project in Chile

BYD Signs 3.5GWh BESS Supply Deal for Grenergy’s Oasis de Atacama Project in Chile In a significant advancement in the renewable energy landscape, BYD, a leading global manufacturer of electric vehicles and energy storage solutions, has secured a contract to supply a 3.5 GWh Battery Energy Storage System (BESS) for Grenergy’s Oasis de Atacama project in Chile. This partnership not only highlights BYD's commitment to sustainable energy but also boosts the operational capabilities of one of Latin America's most ambitious renewable projects. Overview of the Oasis de Atacama Project The Oasis de Atacama project, set against the backdrop of Chile's arid Atacama Desert, is designed to harness solar energy at an unprecedented scale. With a focus on sustainable energy development, the project aims to deliver clean energy to the national grid, contributing to Chile's ambitious renewable energy targets. The region is renowned for its optimal solar conditions, making it a prime location for such large-scale solar installations. The Role of Battery Energy Storage Systems The integration of BYD's 3.5 GWh BESS into the Oasis de Atacama project is pivotal. Battery energy storage systems play a crucial role in stabilizing the power supply from renewable energy sources, which are often intermittent. The BESS will store excess energy generated during peak sunlight hours and release it during periods of high demand or low generation. This capability ensures a more reliable and efficient energy supply, strengthening the resilience of the national grid. Enhancing Renewable Energy Efforts in Chile Chile has been recognized as a leader in renewable energy in Latin America, with significant investments aimed at reducing carbon emissions and enhancing energy independence. The synergy between BYD and Grenergy is set to accelerate these efforts, contributing to a more sustainable and eco-friendly energy landscape in the region. Economic Benefits: The project is expected to generate jobs, boost local economies, and attract further investments in renewable technologies. Environmental Impact: By harnessing solar energy and reducing reliance on fossil fuels, the Oasis de Atacama project will significantly lower greenhouse gas emissions, aligning with global climate goals. Technological Innovation: BYD’s advanced battery technology will deliver high efficiency and durability, making the system well-suited for the challenges associated with large-scale energy storage. Industry Implications The collaboration between BYD and Grenergy serves as a blueprint for future renewable energy projects worldwide. It underscores the growing importance of energy storage solutions in optimizing the performance of renewable energy systems. As the global energy landscape transitions towards more sustainable practices, such partnerships will become increasingly vital. Conclusion The 3.5 GWh BESS supply deal between BYD and Grenergy marks a significant milestone in the realm of renewable energy, particularly in the context of Latin America’s evolving energy infrastructure. As the Oasis de Atacama project moves forward, it will not only enhance Chile’s energy matrix but also set a precedent for future renewable initiatives globally. This partnership exemplifies the potential for innovation and collaboration in addressing the pressing energy challenges of our time, paving the way for a cleaner, more sustainable future.

NanoGraf to launch US's first large-volume silicon oxide factory

Chicago-headquartered NanoGraf Technologies, which claims it has enabled the world’s most energy dense 18650 lithium-ion cell, today announced that it will open the first large-volume silicon oxide factory in the United States. At peak production, NanoGraf will produce 35 tons per year. NanoGraf’s new US high-performance silicon anode materials factory, which is under construction, is in Chicago’s West Loop neighborhood. And, it was a $10 million US Department of Defense (DoD) contract that made this new 17,000-square-foot factory possible. Thanks to the Inflation Reduction Act, NanoGraf will also get a 10% tax credit for domestic anode material production. NanoGraf already had an R&D facility in Chicago, and it’s been piloting its products in Japan. In 2019, the US Council for Automotive Research, a consortium of Ford, General Motors, and Stellantis, provided NanoGraf with $7.5 million for a 36-month electric vehicle battery research and development project. Advertisement - scroll for more content Connor Hund, chief operating officer at NanoGraf, explained why the DoD contract is a milestone for the company in a video call today with Electrek: The Department of Defense is incredibly supportive of US manufacturing, as it’s in the interest of national security. We’re providing lighter batteries for soldiers to carry, and battery cells on soldiers isn’t something the DoD takes lightly. The national security element of domestic battery manufacturing results in bipartisan support. NanoGraf intentionally treads the path of careful growth, and the 18-month contract with the DoD allows NanoGraf to scale up domestic production in a deliberate way. Hund feels it’s that methodical step that lays the groundwork for the company’s next stage of supplying domestically produced batteries to the EV market by 2024 – and that’s when it intends to achieve its goal of producing 1,000 tons of silicon anode material per year. Hund added: Manufacturing is the hardest part – there’s a lot of great technology sitting in labs. The DoD is catalyzing the growth of our company, and we need that growth to be ready for the EV revolution. Senator Dick Durbin (D-IL) said of NanoGraf’s Chicago factory announcement: Illinois is poised to become a leader in the electric vehicle revolution, thanks to leaders in our state like NanoGraf. With its groundbreaking research and production of lightweight, energy-dense batteries, NanoGraf is helping define the next generation of consumer and military vehicles. Read more: This easy-to-use calculator tells you how much money you’ll get from the Inflation Reduction Act Photo: NanoGraf UnderstandSolar is a free service that links you to top-rated solar installers in your region for personalized solar estimates. Tesla now offers price matching, so it’s important to shop for the best quotes. Click here to learn more and get your quotes. — *ad. FTC: We use income earning auto affiliate links. More.

GDI Secures $11.5M in follow-on funding led by Helios Climate Ventures, Impact NY, and InnoEnergy

GDI, a global leader in 100% silicon anodes for advanced lithium-ion battery technology, today announced the successful completion of a major follow-on Series A funding round, led by Helios Climate Ventures, Impact NY, and InnoEnergy, matched with cofinancing in the form of a market-based convertible loan from the Province of Groningen through SIA. Closing over $11.5M in investment from existing and new investors, bringing the total of GDI’s Series A to over $20 million to date. This strategic capital injection accelerates GDI’s mission to scale production of its groundbreaking 100% silicon anodes, leveraging domestic supply chains across Europe and the United States—driving energy independence, resilient supply chains, and job creation. “This milestone enables the next phase of our journey toward transforming the global battery industry,” said Rob Anstey, Founder and CEO of GDI. “We’re advancing more than battery technology, since batteries affect every area of our lives from consumer electronics, medical devices, defense, to electric mobility. We’re building resilience, improving prosperity, national security, and leading to a sustainable energy future.” With this latest round, GDI has launched pilot production in the Netherlands, delivering 300kWh capacity and positioning itself to be a global leader in 100% silicon anode manufacturing. The company will establish its European headquarters in Groningen, Netherlands, strategically located at the heart of the EU energy and innovation ecosystem. “We invest in bold technologies that move the world forward,” said Josh Grehan, Partner at Helios Climate Ventures. “GDI’s scalable, domestic, 100% silicon anode solution aligns perfectly with our mission to drive both climate impact and financial return. Their ability to offer a better battery, without increasing costs is a game changer. We are excited by their partnerships in defense, medtech, consumer, and automotive applications.” “GDI’s silicon anode technology doesn’t just improve battery performance, it addresses Europe’s strategic battery needs,” said Jacob Ruiter, CEO Benelux of InnoEnergy. ” By combining deep scientific innovation with a clear path to manufacturing at scale, GDI is building the foundation for Europe’s and the US’s battery value chains. They help to accelerate a cleaner, more resilient energy system across both sides of the Atlantic.” “The establishment of GDI contributes to the policy vision of the Province of Groningen and the Dutch Ministry of Economic Affairs, aiming at a knowledge-intensive economy, and shows a close fit to goals of the economic agenda Nij Begun” said Sytze Hellinga of NOM. “We are proud to welcome GDI’s European headquarters in Groningen” Driving the Silicon Revolution in Batteries GDI’s patented 100% silicon anode technology solves three long standing barriers to commercializing silicon in batteries: Cycle-life limits from uncontrolled expansion issues Safety concerns from silicon powder and lithium dendrite formation Scalability and high manufacturing cost Their solution enables: Over 30% higher energy density Under 15-minute charging A secure supply chain based on US and European materials and equipment Compatibility with existing large-scale solar and glass manufacturing equipment Direct integration into existing battery manufacturing A Secure, Domestic, and Sustainable Alternative to Graphite Today’s graphite-based anodes face critical limitations: lower energy density, environmental concerns, and dependency on China for over 90% of the critical battery material production. GDI’s silicon technology provides a cleaner, more efficient, and geopolitically resilient alternative—sourced and manufactured domestically. Strong Partnerships for Scalable Manufacturing GDI is collaborating with AGC Plasma Technology Solutions to develop efficient, high-throughput roll-to-roll coaters, a key step in industrial-scale production. Schlenk SE, a leading global foil manufacturer, will supply the copper alloy substrate essential for GDI’s anodes. With 31 patents worldwide, GDI stands at the forefront of battery innovation, ready to enable the future of consumer electronics, defense applications, medical devices and e-mobility. “The future of lithium-ion anodes is silicon—and GDI is making that future scalable, higher performance, and a more affordable reality,” said Anstey. “This funding round is a strong endorsement from investors who deeply understand and believe in our vision and technology.” SIA stands for the Strategic International Acquisition which is a public financial facility related to Nij Begun, executed by the NOM and managed through a partnership between the Province of Groningen and the Dutch Ministry of Economic Affairs. The goal of the SIA is to attract international companies with strategic added value for the regional economy of Groningen and northern Drenthe by being able to offer financial support. gdinrg.com

I threw an e-bike battery into a tub of water to see what happened

The Shocking Truth: What Happened When I Threw an E-Bike Battery in a Tub of Water In recent years, e-bikes have surged in popularity, offering an eco-friendly mode of transport that's both efficient and exciting. With this boom, the safety of lithium-ion batteries—the powerhouses that drive these electric bikes—has become a topic of discussion. Curious about their resilience and potential risks, I decided to conduct an unorthodox experiment: I threw an e-bike battery into a tub of water. Here’s what happened. The Setup Before I embarked on this experiment, I took the necessary precautions: Safety Gear: I donned protective eyewear, gloves, and stood back from the tub to minimize any potential hazards. Controlled Environment: I conducted the test in an open space, away from flammable materials or any surfaces that could be damaged by water. The e-bike battery I used was a lithium-ion type, commonly found in modern electric bikes. Having read about their behavior, especially when damaged or submerged, I was eager to see first-hand the repercussions of tossing one into water. The Experiment I dropped the battery into a large tub filled with approximately 50 gallons of water. Initially, nothing seemed to happen. The battery floated for a few moments before it started to sink slowly to the bottom. I waited, watching with bated breath. The Immediate Reaction As the battery settled, I noticed the following: No Immediate Explosion or Flames: Contrary to what some may expect, there were no immediate signs of combustion or an explosion. The lithium-ion battery remained intact for a while. Bubbles and Fizzing: After a few minutes, small bubbles began to form around the battery. This phenomenon intrigued me. It seemed to suggest that the battery casing might have been compromised. The Surprising Outcome As time went on, the weight of the battery caused water to seep in. The battery eventually became compromised and started to leak a clear, slightly viscous fluid. This was alarming, as it potentially indicated the breakdown of the internal components. In electric batteries, this leakage can often lead to thermal runaway—where a battery overheats and may combust. Aftermath After about 15 minutes, I finally decided to remove the battery from the water, but not before observing a few more details: Corrosion: The exterior of the battery showed signs of rust and corrosion. Despite being waterproof to some extent, prolonged exposure clearly damaged its integrity. Decreased Capacity: The experiment revealed how vulnerable batteries can be. While I couldn’t measure the battery's remaining capacity immediately, it was clear that exposure to water drastically affected its usability. Lessons Learned Never Submerge Lithium-Ion Batteries: Although I conducted this experiment out of curiosity, real-world incidents have shown that submerging lithium-ion batteries can lead to serious safety hazards, including fires and explosions. Water Can Compromise Safety: This experiment clearly illustrated that water and electronics should not mix. The risk of thermal runaway increases significantly when a battery's components are compromised. Safety First: If you're ever dealing with a damaged battery, always prioritize safety. Proper disposal or recycling is crucial to prevent hazards. Conclusion My spontaneous experiment with an e-bike battery provided valuable insights into the behavior of lithium-ion batteries when submerged in water. While it didn't explode as dramatically as some might expect, the potential for danger is undoubtedly there. This experience reinforced the importance of handling battery technology with respect and care. So, if you’re ever tempted to replicate this experiment, I’d strongly advise against it. Safety is paramount, and understanding these powerhouses will help us use them responsibly in our daily lives.

Qbuzz places second order with Yutong

Qbuzz has placed a second order with Yutong for 62 electric buses. This follows the successful deployment of 50 Yutong electric buses in the South Holland North concession, where they went into service in December 2024. The Dutch operator reports strong technical reliability and high satisfaction among both passengers and drivers. “Yutong brings the sustainability goals in South Holland North within reach again,” said Annemarie Zuidberg, General Manager at Qbuzz. “The first results from the customer satisfaction survey that market researcher Newcom is conducting on our behalf also show a higher passenger appreciation for comfort, luxury and overall travel experience.” Qbuzz does not specify which model it opted for. However, the previous order was for the Yutong U15, a 15-metre electric bus that has room for about 100 passengers. Qbuzz’s latest procurement decision reflects wider challenges in Europe’s electric bus market. The company previously faced major disruptions, including delivery setbacks from Iveco and the bankruptcy of Van Hool, which led to the cancellation of an order for 112 electric buses. In contrast, Yutong was able to manufacture and deliver 50 units within six months, meeting both technical and operational benchmarks, said Qbuzz. With Dutch concession providers demanding increasingly ambitious decarbonisation targets, Qbuzz emphasises a pragmatic approach—balancing availability, price-performance and supplier reliability. The new Yutong buses are expected by the end of 2025, marking another step toward fully electric public transport in the Netherlands. qbuzz.nl (in Dutch)

Global battery storage deployments hit nearly 9 GWh in April, says Rho Motion – pv magazine International

China and Chile led battery storage deployments in a more evenly distributed scene than in previous months, but a lower overall total was installed at grid-scale. May 21, 2025 Tristan Rayner From ESS News Market intelligence firm Rho Motion, the downstream arm of Benchmark Mineral Intelligence, says it tracked nearly 9 GWh of new global battery energy storage system (BESS) capacity entering commercial operations in April 2025. This came from a total of 3,333 MW/8,890 MWh of grid-scale projects. According to Rho Motion’s “Battery Energy Stationary Storage Monthly Database,” this April capacity is 13% higher than in the same period in 2024, though it marks the lowest deployment month in 2025 so far, potentially due to industry seasonality. The data also indicates that global deployments were more evenly distributed across geolocations than during the first quarter of the year. To continue reading, please visit our ESS News website. This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com. Popular content

Trump’s Tariffs Are Wrecking America’s Supply Chain for Critical Minerals

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and/or follow us on Google News! The Trump administration’s latest round of tariffs is drawing scrutiny, but the real concern isn’t just the cost of Chinese EVs—it’s the impact on the materials those tariffs affect. Nickel, cobalt, and platinum-group elements (PGEs) are indispensable to the U.S. economy, yet the country is overwhelmingly reliant on imports, often from nations it is now targeting with trade restrictions. These metals power everything from electric vehicle batteries to jet engines and oil refineries, but the new tariffs raise questions about whether the U.S. is inadvertently deepening its supply chain crisis. Lyle Trytten, better known as ‘The Nickel Nerd,’ recently highlighted the issue on LinkedIn, noting that the U.S. has now placed itself at odds with countries that supply 60 to 80 percent of its nickel, cobalt, and PGEs. With Canada, Mexico, China, Europe, and South Africa all facing some degree of friction, the supply chains underpinning critical industries are under strain. The question now is not whether disruptions will occur, but how severe the consequences will be. The United States currently depends on foreign sources for between 70 and 100 percent of its supply of these critical minerals. Nickel, essential for stainless steel and lithium-ion batteries, is primarily sourced from Indonesia, the Philippines, Canada, and Russia, with Indonesia alone accounting for over a third of global production. Cobalt, used in aerospace alloys and electric vehicle batteries, is overwhelmingly mined in the Democratic Republic of Congo (DRC), which supplies over 70 percent of the world’s output, before being refined predominantly in China. The United States has historically relied on imports from Canada, Norway, and Australia for cobalt, but these sources account for only a fraction of the total demand. PGEs, including platinum, palladium, and rhodium, are primarily produced in South Africa, which supplies nearly 70 percent of global platinum output, and Russia, which has dominated palladium production for decades. Zimbabwe has also emerged as a notable supplier of PGEs, though its exports remain relatively small in comparison. The supply chains for these minerals are not only fragile but concentrated in the hands of a few countries, making them highly vulnerable to geopolitical shifts, trade restrictions, and export controls. Trade disputes have already placed significant pressure on these supply chains. The Trump administration’s 2025 tariff proposals — aimed at bolstering domestic manufacturing, punishing weaker countries, boosting the Presidential ego or some combination of the above — have further complicated the situation. While tariffs on nickel, cobalt, and PGEs have been discussed, there remains uncertainty over whether they will be fully implemented or only selectively applied. Some sources suggest that duties on refined nickel from China and Russia are all but certain, while others indicate that tariffs on PGEs and cobalt remain under debate due to potential industry backlash. Even where tariffs have not yet been enacted, industries must prepare for them, as businesses must factor in trade policy risks when planning supply chains. The result is that between 60 and 80 percent of America’s imports of nickel, cobalt, and PGEs now come from countries with which relations are strained. Canada and Mexico, traditionally stable suppliers, have faced increasing trade friction, while allies in Europe are pushing back against broader U.S. industrial policies. South Africa, though not directly embroiled in the tariff debate, remains a wildcard in the long-term reliability of supply. Regardless of whether full tariffs take effect, the lack of clarity itself is causing disruption, forcing manufacturers to seek alternative sources, reconsider supply agreements, and assess the long-term viability of relying on imported materials. If current tensions escalate further, the economic impact will be profound. The automotive industry, already dealing with supply chain disruptions and rising costs, could see EV battery prices surge as nickel and cobalt become more expensive. Nickel is a crucial component of lithium-ion battery cathodes, particularly in high-performance batteries used in long-range electric vehicles. Cobalt, while increasingly being reduced in battery chemistry, remains an important stabilizer, ensuring battery longevity and safety. Most of the world’s nickel supply comes from Indonesia, Russia, and Canada, while cobalt is overwhelmingly sourced from the Democratic Republic of Congo and refined in China. Shifting to alternative suppliers like Australia or Brazil is possible but would take years of investment in new refining capacity. The aerospace sector, which relies on cobalt-based superalloys for jet engines and gas turbines, would face similar pressures. Cobalt’s high-temperature resistance makes it indispensable for aircraft engines, military jets, and space applications. The current leading suppliers of aerospace-grade cobalt are Canada and Norway, but with refining controlled largely by China, rerouting supply chains is complicated. If cobalt prices rise or availability shrinks, aircraft manufacturers could face higher costs, production delays, or even difficulties securing necessary materials. Unlike the automotive sector, where battery chemistries can evolve to reduce cobalt dependence, aerospace alloys have few substitutes, making them particularly vulnerable to supply shocks. Oil refineries and chemical manufacturers, which depend on PGEs for catalysts, could see production costs rise, potentially increasing gasoline and consumer goods prices. Platinum, palladium, and rhodium are essential for refining crude oil into gasoline and petrochemicals, as well as for manufacturing fertilizers, medical equipment, and advanced polymers. The vast majority of PGEs come from South Africa and Russia, with smaller contributions from Zimbabwe and Canada. Finding alternative sources for PGEs is difficult because these elements are rare and often mined as byproducts of other metals, meaning production cannot be quickly scaled up elsewhere. Inflation, already a persistent concern, could be further exacerbated by soaring raw material costs. Rising prices for nickel, cobalt, and PGEs will trickle down into consumer goods, including electronics, vehicles, and industrial equipment. Without stable supply chains or alternative sources, American manufacturers may struggle to maintain competitive pricing, leading to economic pressure across multiple sectors. Whether through increased costs passed on to consumers or potential slowdowns in production, the impact of disrupted mineral supply chains

Changan opens its first full-fledged overseas NEV plant in Thailand

Changan Opens Its First Full-Fledged Overseas NEV Plant in Thailand In a significant move reflecting its commitment to global expansion and the burgeoning electric vehicle market, Changan Automobile has inaugurated its first full-fledged overseas New Energy Vehicle (NEV) plant in Thailand. This landmark event marks a pivotal moment for Changan as it seeks to enhance its international footprint in the rapidly evolving automotive sector. Investment and Development Changan's new plant in Thailand represents a substantial investment aimed at tapping into Southeast Asia's growing demand for electric vehicles. The facility is designed to produce a range of NEVs that cater to both local and international markets, underscoring Changan's strategy to leverage regional manufacturing capabilities while promoting sustainable mobility solutions. The plant is equipped with state-of-the-art technology, focusing on high-efficiency production processes that align with global standards. This aligns with Thailand's ambition to become a regional hub for electric vehicle manufacturing, complementing the government's efforts to promote environmentally friendly transportation. Strategic Importance Thailand's strategic location within Southeast Asia provides Changan with access to emerging markets and a skilled workforce. The plant is expected to support local economies, create jobs, and stimulate technological advancements in the automotive sector. With increasing investment in electric vehicle infrastructure, including charging stations and incentives for EV adoption, Thailand is becoming an attractive destination for automotive companies focused on sustainability. Changan's presence in Thailand not only strengthens its competitive position but also enhances collaboration with local suppliers and stakeholders, thereby fostering innovation in the NEV space. Focus on Sustainability As global concerns about climate change escalate, the automotive industry is poised for a significant transformation. Changan's commitment to sustainability is reflected in its production of NEVs, which are designed to reduce emissions and promote a greener future. The company aims to incorporate renewable energy solutions within the manufacturing process, further minimizing its carbon footprint. The introduction of NEVs to the Thai market aligns with the country's goals of reducing greenhouse gas emissions and promoting the use of cleaner transportation options. By producing vehicles tailored to local needs, Changan is not only contributing to environmental sustainability but also enhancing mobility for Thai consumers. Future Prospects Looking ahead, Changan's strategic investment in Thailand signifies its long-term vision for growth within the NEV landscape. As consumer preferences shift towards sustainable transportation solutions, the company is well-positioned to capitalize on the increasing demand for electric vehicles. The success of the Thailand plant may pave the way for further international expansions, as Changan continues to explore opportunities in other markets. With a focus on innovation, sustainability, and local collaboration, Changan aims to solidify its position as a leader in the global NEV industry. Conclusion Changan Automobile's inauguration of its first fully overseas NEV plant in Thailand is a landmark achievement that exemplifies the company's commitment to global expansion and sustainability. By investing in local manufacturing and aligning with Thailand's vision for a greener future, Changan is set to make a significant impact in the electric vehicle market, contributing to both economic growth and environmental sustainability. As the automotive industry continues to evolve, Changan's strategic initiatives position it as a key player in the transition towards electric mobility.

Halifax adds 60 electric buses to public fleet

The operator, which serves the city of Halifax in Nova Scotia, first put out a tender for the procurement of 60 electric buses back in 2021. Nova Bus emerged as the winner of the tender, with buses meant for delivery by 2024. According to Halifax Transit, the first Nova LFSe+ was delivered in December 2023 and used for initial testing, training and PR. Following that, the other 59 electric buses were delivered within 12 months, with real-world in-service testing of three buses beginning in December 2024. However, all 60 electric buses have now been commissioned for regular service, along with the associated charging infrastructure. Funded by $112m CAD (~€71m) from the governments of Canada, Nova Scotia, and the city itself, Halifax Transit expanded its Ragged Lake Transit Centre (RLTC). The firm added 40 additional parking spaces for buses as well as 67 charging stations with a total maximum capacity of up to 5,250kW. This is supported by the installation of a solar array on the roof of the building. The buses themselves will have the same passenger capacity as current diesel models. However, they are reportedly much quieter and therefore fitted with an altering system that sends ‘unobtrusive warning sounds’ at slower speeds. Additionally, the buses use a regenerative braking system to conserve charge. Halifax Transit now plans to expand its fleet to a further 200 zero-emission buses over the coming years, but is yet to commit to a specific powertrain. The mayor of Halifax, Andy Fillmore, has, however, stated that the city is also exploring the use of natural gas and hydrogen-powered buses, specifically in areas where BEVs are unfeasible due to weather conditions. Anthony Edmonds, project manager of fleet electrification for Halifax Transit, told CBC: “It’s incredibly exciting. We’ve been working towards this for a long time and to finally be able to cut the ribbon on this new facility, I think it’s a big milestone for Halifax Transit. I think it’s a sign of more things to come and the start of a really bright, green future.” halifax.ca, cbc.lite.ca, ctvnews.ca

EU backs 15 hydrogen projects – pv magazine International

The European Commission has selected projects for €992 million ($1.1 billion) of EU public funding, while the Japanese government has agreed to provide $4.80 in subsidies for hydrogen fuel cell trucks. May 21, 2025 Sergio Matalucci The European Commission has selected 15 renewable hydrogen production projects for €992 million in EU public funding across the European Economic Area (EEA). “The projects, located across five countries, are expected to produce nearly 2.2 million tons of renewable hydrogen over ten years,” said the European executive body. Eight projects will be in Spain, three in Norway, two in Germany, one in Finland, and one in the Netherlands. The biggest projects in terms of bid capacity are one in the Netherlands, followed by one in Germany. In terms of bid price, seven out of the eight cheapest hydrogen projects are in Spain. The funds will come from Innovation Fund, sourced from the EU Emissions Trading System (ETS). The European Union, which recently decided to continue technical regulatory exchanges on hydrogen with the United Kingdom, has published its opinion on the statutory documents of the European Network of Network Operators for Hydrogen (ENNOH), the association representing future hydrogen transmission network operators at the EU level. The European Commission said the operators must adopt and publish the final statutory documents by early July 2025, incorporating feedback from both the Commission and the Agency for the Cooperation of Energy Regulators (ACER). The Japanese government has agreed to subsidize hydrogen for fuel cell trucks and buses in six prefectures, with the subsidy set at JPY 700 ($4.80)/kg, according to Nikkei. Government official Shinichi Kihara said at the World Hydrogen Summit in Rotterdam that Japan’s contracts-for-difference (CfD) program for clean hydrogen has been oversubscribed, with project selection expected to begin in the latter half of the fiscal year. Japanese and German officials also met in Rotterdam to discuss hydrogen demand creation and financing. Infinium has selected Electric Hydrogen’s 100 MW solution for its large-scale eFuels facility in Texas. “Electric Hydrogen’s HYPRPlant is a complete solution that lowers hydrogen total installed project cost by up to 60% relative to other electrolyzer solutions,” said Electric Hydrogen, which produces the system between Massachusetts and Texas. Electric Hydrogen said that its modular manufacturing approach makes the HYPR plant “less expensive and more reliable” than imported Chinese products. KK Wind Solutions has agreed to supply 10 customized power supply units for Sunfire’s 100 MW pressurized alkaline electrolyzer, with each unit including transformers, rectifiers, AC connections, and cooling systems. It previously delivered two units for Sunfire’s 10 MW pilot electrolyzer in 2023, each consisting of a 5 MW rectifier and a transformer. KK Wind Solutions said the experience from that project was critical to scaling the power supply units to 10 MW for full-scale green hydrogen production. This content is protected by copyright and may not be reused. If you want to cooperate with us and would like to reuse some of our content, please contact: editors@pv-magazine.com. Popular content

Powering Healthcare: Innovations in Medical Device Battery Technology

Introduction As healthcare continues to integrate technology, the demand for reliable and innovative power solutions grows. Medical devices are at the forefront of this evolution, requiring advanced battery technologies to ensure efficiency and reliability. This article explores the latest innovations in medical device battery technology, highlighting their significance in the healthcare sector. The Importance of Battery Technology in Healthcare Battery technology plays a pivotal role in the operation of medical devices. From portable monitors and infusion pumps to wearable health trackers, these devices rely on batteries to deliver critical healthcare services without interruption. The right battery technology can enhance the performance, safety, and usability of medical devices. Recent Innovations in Medical Device Battery Technologies 1. Lithium-Sulfur Batteries Lithium-sulfur (Li-S) batteries are emerging as a front-runner in medical device applications due to their high energy density and lightweight nature. Unlike conventional lithium-ion batteries, Li-S batteries can store more energy, making them ideal for devices requiring long operational times between charges. 2. Solid-State Batteries Solid-state batteries offer a significant advancement over traditional lithium-ion technology. They utilize a solid electrolyte instead of a liquid one, reducing the risk of leaks and improving safety. This innovation can lead to longer-lasting and more efficient batteries for medical devices. 3. Wireless Charging Technology Wireless charging solutions are becoming increasingly popular in the healthcare industry. This technology allows devices to be charged without physical connections, minimizing wear and tear on charging ports and improving hygiene—crucial factors in hospital settings. 4. Energy Harvesting Techniques Energy harvesting techniques, such as piezoelectric systems and thermoelectric generators, convert ambient energy into electrical power. This innovation can provide a continuous power supply for medical devices, reducing dependency on batteries and enabling devices to operate indefinitely. Challenges and Considerations While advancements in battery technology present numerous opportunities, there are challenges to consider. Regulatory approvals, battery lifespan, and the environmental impact of battery disposal are critical factors that must be addressed as new technologies are developed and implemented. The Future of Medical Device Battery Technology The future of battery technology in healthcare looks promising, with ongoing research and development focusing on enhancing energy efficiency, longevity, and safety. As medical devices become increasingly sophisticated, the need for advanced battery solutions will continue to grow, driving innovation in this vital area of healthcare technology. Conclusion Innovations in medical device battery technology are crucial for improving healthcare delivery. By enhancing the reliability and functionality of medical devices, these advancements contribute to better patient outcomes and a more efficient healthcare system. As the industry continues to evolve, staying informed about battery technologies will be essential for both healthcare providers and manufacturers alike.

Grunge Meets Grid: How Pearl Jam’s Carbon Price Led Me to Battery ETFs

Sign up for CleanTechnica's Weekly Substack for Zach and Scott's in-depth analyses and high level summaries, sign up for our daily newsletter, and/or follow us on Google News! Last Updated on: 13th April 2025, 08:55 pm The world is electrifying at an accelerating pace, and while solar panels and wind turbines grab most of the headlines, the real power behind the transition lies buried in rocks and embedded in chemistry. Batteries and the critical minerals that go into them are the plumbing of the clean energy transition. They’re not the shiny bits on rooftops or the turbines on hills, but the essential connective tissue that makes decarbonized transport and renewable-powered grids work. And in a world where governments, automakers, and utilities are all betting big on electrification, long-term investors are asking the right question: How can we get meaningful, diversified, fossil-free exposure to the core of this transformation? At least, that’s the question I’m asking as I rebalance my personal portfolio, and a question I was recently asked by Pearl Jam. That’s right, the grunge rock heavy hitter recently reached out to me to ask how they could invest their personal carbon pricing of their concert travels at $200 per ton. They’ve been doing that for a long time, with guitarist Stone Gossard leading that focus. Their efforts have included supporting projects like Amazon rainforest reforestation, sustainable fuels, and photovoltaic technology. For instance, during their 2018 US and European tours, they offset approximately 3,500 tons of CO₂ emissions through conservation work on Afognak Island in Alaska, home to old-growth coastal temperate rainforests. But when they reached out, they were pivoting a bit. Like pretty much everyone, they’ve realized that it’s possible to invest in the future and get a financial return. A mutual contact knew of my work assessing startups, dissecting portfolios like those of Breakthrough Energy Ventures (far too many obvious thumbs down investments), and advising investment funds, and connected us. One answer I’ve been looking at is exchange-traded funds (ETFs) that focus on batteries and critical minerals. Unlike individual mining stocks or battery startups, these ETFs package multiple exposures into one instrument, spreading risk across geography, company maturity, and position in the supply chain. For investors with a buy-and-hold mindset who want to back the structural drivers of electrification without dancing in and out of speculative trades like me, these ETFs can be strategic anchors. But not all ETFs are created equal, and even fewer tick the boxes of global diversification, cleantech purity, and meaningful exposure to China’s dominant players. Note a couple of things: I’m not a registered financial advisor and this isn’t me telling you to invest in something. That’s for you to decide with your advisers. This is me as an informed person doing my own quixotic research for my own portfolio and sharing the results. Let’s start with equity ETFs, because for most investors, they are the most accessible and straightforward path to long-term thematic exposure. Three ETFs stand out: Global X Lithium & Battery Tech (LIT), VanEck Rare Earth/Strategic Metals (REMX), and Amplify Lithium & Battery Tech (BATT). Each covers a different segment of the battery value chain, and each comes with its own risk profile. LIT is the flagship lithium and battery tech ETF, with about 47% of its portfolio in Chinese companies like CATL, BYD, and Ganfeng Lithium. It provides exposure across the full lithium cycle, from mining to refining to battery production. Its five-year annualized return clocks in at an impressive 13.1%, albeit with serious volatility—a peak in late 2021 followed by a sharp pullback that wiped out more than half its gains. Still, for long-term holders, it’s been a rewarding ride. The fund charges a 0.75% expense ratio, higher than average but justified by its targeted exposure and deep liquidity. It’s a core holding for anyone serious about lithium and battery technologies. REMX, by contrast, is a deep dive into critical minerals, especially rare earth elements. It has roughly 29% exposure to Chinese firms and focuses on miners and refiners of strategic metals like neodymium, praseodymium, and tungsten—essential for EV motors, wind turbine magnets, and defense technologies. It’s not a battery ETF per se, but a pure play on the raw material scarcity that underpins cleantech. Its five-year annualized return sits at around 9.4%, and its expense ratio is a modest 0.56%. Volatility is high, with a 60% drawdown from its 2021 peak, but the thesis is strong: these metals are rare, geopolitically sensitive, and increasingly valuable. BATT takes a broader approach. With about 33% of its portfolio in Chinese companies, it includes not just lithium miners and battery manufacturers, but also EV automakers, charging networks, and next-gen battery startups. Its five-year annualized return is around 7.1%, and it charges a 0.59% fee. BATT is a bit more diluted in focus, and its inclusion of pre-profit EV firms introduces speculative risk, but it offers breadth that the other two lack. For those wanting diversified exposure across the EV value chain, it serves a useful role. As a note on the focus on China exposure, frankly, I’d like it to be higher, but these are the ETFs available to western investors. China is heavily dominating the battery industry globally and is investing far more in battery innovation than the rest of the world. They own the battery minerals industry as well. I’d rather have higher exposures to them, but without getting into picking individual stocks, this is what I have. And further, Europe and North America are attempting, with fits, starts, setbacks, and some wrong-headed plays like Northvolt, to reshore at least some battery manufacturing. Here’s how the equity ETFs compare: ETF Focus China Exposure MER 5-Year Return LIT Lithium value chain ~47% 0.75% +13.1% annualized REMX Critical minerals ~29% 0.56% +9.4% annualized BATT Broad battery & EV ~33% 0.59% +7.1% annualized Equity ETFs are only half the story. The other half is commodity ETFs—those tracking the prices of metals themselves, rather than the companies that extract or refine